These are shares that have been bought back by the company either because it has no further use for them or because they think the stock is undervalued and represents a good investment. Treasury Stock is credited for the total cost of the shares sold, and the account Additional Paid-in Capital from the Sale of Treasury Stock Above Cost is credited for the difference. By purchasing shares from stockholders, the corporation can use them, for example, as part of the compensation to executives without having to go through the legal difficulties of amending the Charter to allow additional shares to be issued. A corporation’s board of directors may decide to acquire treasury shares for various reasons. One reason for this action is to obtain shares for re-issuance when all authorized shares are issued and outstanding.

Get in Touch With a Financial Advisor

To record a repurchase, simply record the entire amount of the purchase in the treasury stock account. Hence, the fully diluted shares outstanding count is a relatively more accurate representation of the actual equity ownership and equity value per share of a company. In effect, the TSM estimates the hypothetical impact of the exercising of in-the-money securities to measure their collective effect on the fully diluted shares outstanding.

2: Analyze and Record Transactions for the Issuance and Repurchase of Stock

- Treasury stock transactions have no effect on the number of shares authorized or issued.

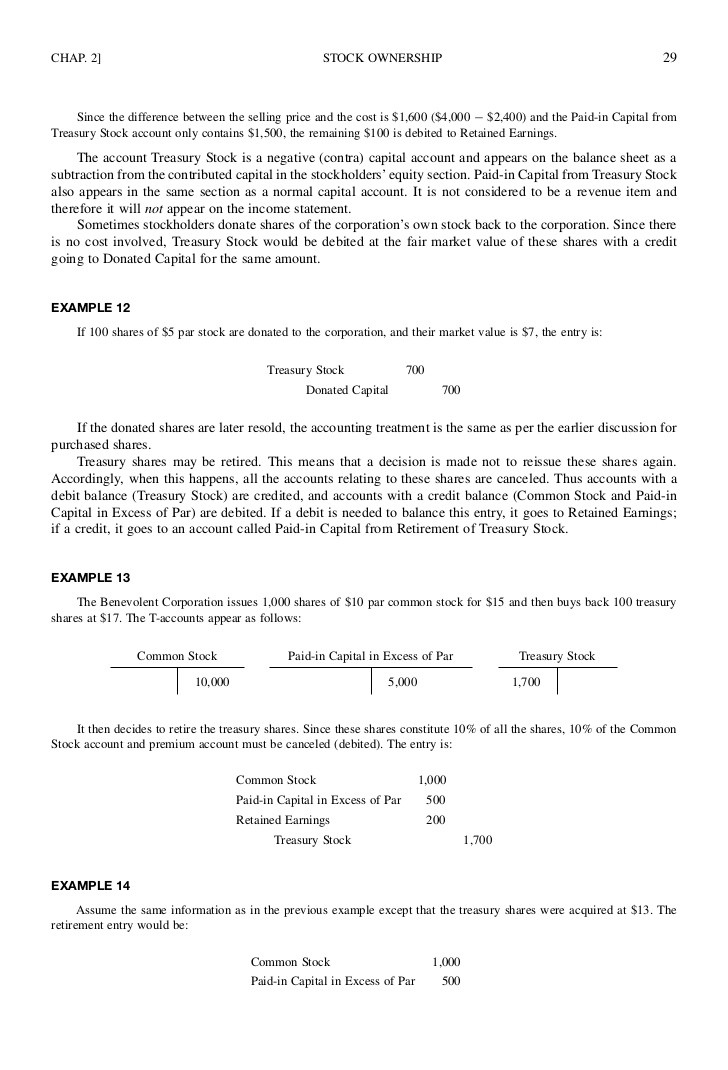

- The Treasury Stock account decreases by the cost of the 100 shares sold, 100 × $25 per share, for a total credit of $2,500, just as it did in the sale at cost.

- In computing earnings per share (EPS), treasury stock is not considered outstanding and must be deducted when determining the weighted average number of shares outstanding.

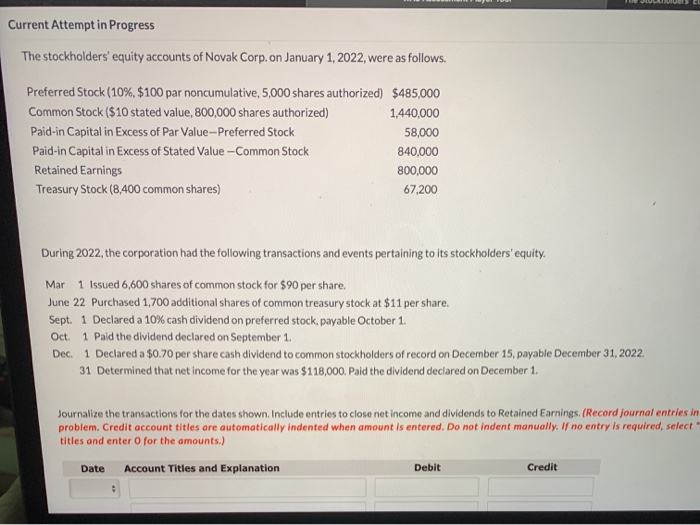

- Journalize the above transactions according the par value method of accounting for treasury stock.

- Let’s assume that the average market price for the shares in the last year was $100.

Once the shares of the company are issued, the company cannot regulate who owns their shares. However, some times, companies may choose 13 9 items reported on a corporate income statement to repurchase their shares from its shareholders. The company can choose to either retire these shares or resell them in the future.

Why You Can Trust Finance Strategists

Even though the difference—the selling price less the cost—looks like a gain, it is treated as additional capital because gains and losses only result from the disposition of economic resources (assets). Assume that on August 1, La Cantina sells another 100 shares of its treasury stock, but this time the selling price is $28 per share. The Cash Account is increased by the selling price, $28 per share times the number of shares resold, 100, for a total debit to Cash of $2,800. The Treasury Stock account decreases by the cost of the 100 shares sold, 100 × $25 per share, for a total credit of $2,500, just as it did in the sale at cost. The difference is recorded as a credit of $300 to Additional Paid-in Capital from Treasury Stock. To comply with generally accepted accounting principles (GAAP), the treasury stock method must be used by a company when computing its diluted EPS.

Par Value vs. Market Value: What’s the Difference?

Any profits or losses are distributed among the partners depending on a set percentage. The percentage of profits or losses attributable to a single partner is decided when the partnership agreement is signed. Every time a partner joins or leaves the business, the partnership agreement is renewed. Get instant access to video lessons taught by experienced investment bankers.

When a company initially issues stock, the equity section of the balance sheet increases through a credit to the common stock and the additional paid-in capital (APIC) accounts. The common stock account reflects the par value of the shares, while the APIC account shows the excess value received over the par value. Treasury stock transactions have no effect on the number ofshares authorized or issued.

Even though the company is purchasing stock, there is no assetrecognized for the purchase. Immediately after the purchase, the equitysection of the balance sheet (Figure14.6) will show the total cost of the treasury shares as adeduction from total stockholders’ equity. Even though the company is purchasing stock, there is no asset recognized for the purchase.

Once retired, the shares are no longer listed as treasury stock on a company’s financial statements. Non-retired treasury shares can be reissued through stock dividends, employee compensation, or capital raising. If the board elects to retire the shares, the common stock and APIC would be debited, while the treasury stock account would be credited. Par value method of accounting for treasury stock is one of the two techniques of accounting to record the purchase and resale of treasury stock.

Add Your Comment